Few of us really like uncertainty. It fills us with dread. It frustrates our planning efforts. It makes analyzing its effects complex. After all, where in a spreadsheet do you put uncertain values for revenue or costs? Admittedly, accounting for uncertainty can be difficult, but doing so can add a lot of value to your business decisions. Let me explain…

The problem: “how do we communicate the value?”

A colleague recently took on the opportunity to broker the sale of a resort hotel. The hotel was recently refurbished and now operates profitably at an approximate 69% occupancy rate for an average nightly room rate of $219. It also gathers a healthy food & beverage income as well as rental income from stores that operate on the promenade level.

The sellers offered the hotel at a premium price, arguing that the refurbishments and marketing/operating strategy that they will pursue (part of the deal is that they will continue to operate the property) will continue to grow the occupancy rate to a target 72% and the room rate to $275/night. Unfortunately, the hotel has been slow to close a deal, so now the sellers want to add a sweetener to their offer: for the next five years, the hotel EBITDA (earnings before interest, taxes, depreciation, and amortization) will return 4% on the sale price of the hotel; if it doesn’t, the sellers will make up the shortfall. “Rob, how do we communicate the value of the guarantee?”

The solution: account for uncertainty

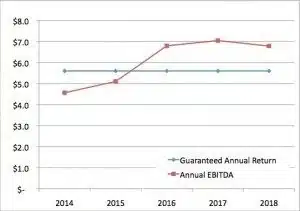

Notionally, the answer to my colleague’s question would be that the value of the guarantee is the sum of the present value of the shortfalls from the guaranteed annual return. In fact, the current forecast pro forma of the hotel includes the EBITDA with the anticipated rates of growth in the occupancy and room rates. If the hotel sold on January 1, 2014, the EBITDA compared to the guaranteed return would look like the following:

At first, the EBITDA falls below the Guaranteed Annual Return, but it catches up with it after the second year…or does it? (Figures in millions)

The value of the shortfall (where the red curve falls below the blue) in this best guess scenario is $1.5 million. But there’s a problem with this analysis. Can you guess what it is?

You’re right. The analysis does not include the likelihood that the hotel seller/operators will achieve the desired, targeted rates of growth. Maybe the market won’t absorb the additional $56/night. Or maybe another recession will wreck the resort industry again. Or maybe the occupancy rates are nearing their natural absorption for the value the hotel offers so that the additional 3% lift on the current rate is a long shot. Some, all, or more of these caveats could come to bear on the owners and operators over the next five years.

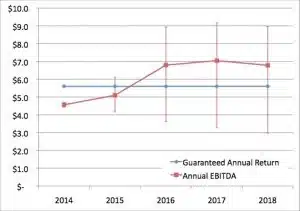

By carefully calibrating the range of uncertainties for the key business model parameters and by using Monte Carlo simulation in an Analytica model, we discovered that the likely range of outcome around the average EBITDA (indicated by the error bars around the Annual EBITDA) probably looks more like this:

The potential range in the EBITDA may still overlap the Guarantee in later years. The guarantee continues to provide value. (Figures in millions)

The potential range in the EBITDA may still overlap the Guarantee in later years. The guarantee continues to provide value. (Figures in millions)

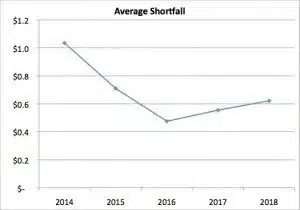

The result is that the average of the potential annual shortfall is much greater than originally anticipated:

The average shortfall exists because there are some futures in which it’s possible that the EBITDA fails to overcome the return guarantee. This information is lost by using single point analysis. (Figures in millions)

When we perform our original value calculation on the large number of possible futures with their probability weighted prevalence in our simulation, we now find that the value of the guarantee is most likely between $1.1 million and $7.2 million (the 80th percentile interval), with an expected value of $3.4 million!

The conclusion: There is value in uncertainty

What did we learn from this analysis?

- The value of the guarantee is actually 2.2 times more valuable than the original analysis implied by not including uncertainty.

- The value of including the uncertainty in the analysis is the difference between the value with uncertainty less the value without uncertainty. In this case, the value of including uncertainty in the business case analysis is $1.9 million (i.e., $3.4 million – $1.5 million).

- The sellers possess both the reasonable and ethical capability to communicate a much better value of their guarantee to a potential buyer.

- The sellers recognize that they likely face more exposure with their guarantee than they originally assumed, and they know the quantity and likelihood of different levels of exposure. Now they can adjust the terms of their guarantee or plan how they can hedge against the exposure.

None of us possess perfect knowledge about the future, but masking that shortcoming with single point analyses introduces another source of risk by inattention. By explicitly addressing and categorizing what we do not know, we can actually discover more sources of value and risk that we previously overlooked. The result? We pick up found money, reduce the anxiety associated with lingering doubts about what may come, and make better plans to hedge the risks that threaten our wealth.

Other references worth considering:

- Expected value of including uncertainty

- Henrion, M. (1982). The value of knowing how little you know: The advantages of a probabilistic treatment of uncertainty in policy analysis (Ph.D. thesis). Carnegie Mellon University.

- Lumina’s webinar from April 2021